Do you know that since September 1st, 2022, off-label cancer drugs are not covered by your MediShield Life? The Ministry of Health has introduced a Cancer Drug List (CDL) consisting of clinically proven and cost-effective cancer treatments. From now on, only treatments listed in the CDL will be claimable under MediShield Life (MSHL), MediSave (MSV), and Integrated Shield Plans (IPs). And from April 1st, 2023, off-label cancer drugs will not be covered by your Integrated Shield Plans (IPs) for both new policies and policy renewals.

According to a study conducted by the Singapore Actuarial Society in 2020, approximately 69% (2.81 million) of Singapore’s population owns an IP. As the deadline approaches and insurers begin to implement changes, there has been a growing concern about the impact of this change. In this article, we will explore the implications of these revisions and how they can affect you and your loved ones.

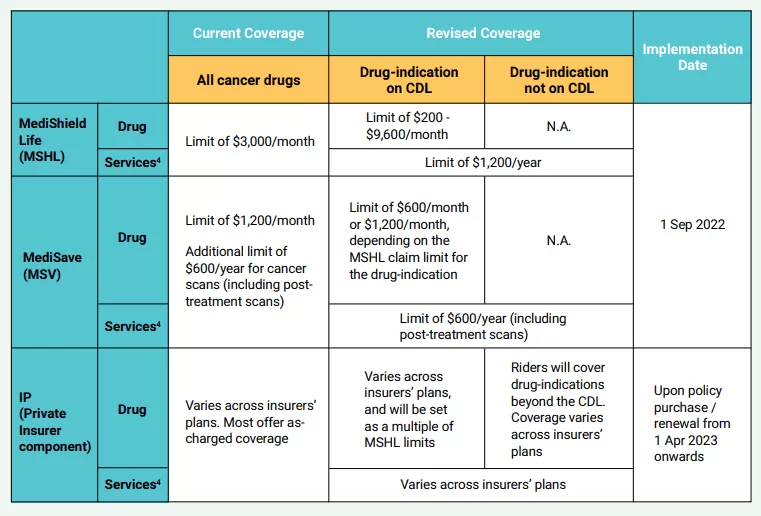

MediShield Life’s Structural Changes

Previously, MediShield Life provided coverage for ALL cancer drugs, with a flat limit of $3,000 per month. However, since September 1st, 2022, the policy has been updated to include the following changes:

- A new Cancer Drug List (CDL) for pre-approved cancer drugs

- Treatments not approved by HSA as a specified treatment for the particular cancer will not be included in the CDL (non-CDL)

- Separation of cancer drug costs and cancer drug services such as consultations, scans, lab investigations, chemotherapy preparation and administration, supportive care drugs, and blood transfusions.

The diagram below shows the changes at a glance.

Let’s take a closer look at the changes and what they mean for patients.

1. Potentially higher coverage for those in Cancer Drug List (CDL)

Firstly, it seems like a positive move to change to tier-based coverage for different cancer drugs instead of a maximum cap per month. This means that potentially, individuals using a drug at the highest tier could claim up to $9,600 per month for the cost of the drug, and up to $1,2,00 $3,600 per year for drug services. This could help manage the cost of drugs and encourage suppliers to price them reasonably according to the specific tiers they fall under.

2. Removal of drugs not in Cancer Drug List (CDL)

However, the removal of drugs not in the Cancer Drug List may not sit well with some patients. Although the government is committed to helping those who are currently using them, the hope is that the approved list of cancer drugs will continue to grow at a pace that can help patients. The Ministry of Health and Health Sciences Authority should work closely together to identify trends and research studies from overseas, approving cancer drugs that can be effective even if there are no local incidents.

3. Seemingly low limits on Cancer Drug Services

The annual limit of $1,200 for Cancer Drug Services seems insufficient, especially for patients requiring frequent tests. It’s reassuring to hear that this limit will increase to $3,600 from April 1st, 2023. However, this limit should be reviewed more intensively to ensure that it covers most situations.

4. IP have no choice but to follow suit

Insurers of Integrated Shield Plans have no choice but to follow exactly what MOH instructs them to do, which includes removing coverage for drugs not on the CDL and setting coverage as a multiple of the MSHL limit. Insurers can offer this coverage by adding on to existing riders or offering additional riders. Although every company offers somewhat different coverage, it’s likely that the coverage across different insurers will start to align over time.

What’s next for consumers?

It remains to be seen how substantial this change will be and how much of an impact it will have on patients’ treatment and overall well-being. At our end, we can ensure that we have a holistic risk-management plan in place to take care of different scenarios that may disrupt our finances and our lives. If you’re not sure of the different types of plans available out there, here is an article you can refer to.

Seek Professional Help

Navigating the changes to CDL and maintaining an optimal insurance portfolio can be daunting tasks. With healthcare trends constantly evolving, it’s important now more than ever to review your policies regularly with a financial planner who can help identify risks and propose independent solutions that are tailored to your needs. It’s also essential not to rely on one type of insurance plan as unforeseen circumstances may arise where certain plans do not cover specific treatments. At times like these, having a comprehensive insurance portfolio will ensure you have adequate coverage, flexibility, and minimise any potential gaps.

If you’re struggling to navigate these challenges or have any questions about managing your insurance portfolio effectively, consider reaching out to me for professional guidance. We’ll walk through your unique situation, and I can come up with personalised and help create a comprehensive strategy that meets all of your needs.

Don’t leave the future of yourself or loved ones up in the air – take action today.

Disclaimer: The content in this article is intended for educational purposes and all personal opinions are not to be taken out of context. Please seek formal advisory consultation for specific holistic planning for you.

References:

1. https://actuaries.org.sg/sites/default/files/2021-01/SASResponseMSHLReview2020FINAL.pdf

2. https://www.straitstimes.com/singapore/health/ong-ye-kung-changes-to-cancer-coverage-should-reduce-cost-of-treatment

3. https://www.straitstimes.com/singapore/insurance-coverage-for-cancer-services-to-go-up-from-april-following-public-feedback-on-coverage-changes-in-2022